Web 2.0 technologies have given rise to a number of new business models and transformed a wide variety of sectors. One of these latest business models is the decentralized online peer?to?peer lending marketplace, in which individual lenders submit bids to lend to individual borrowers seeking microloans, without the intervention of a bank or any centralized financial intermediary. A few interesting technological features differentiate this decentralized online lending market from traditional lending contexts.

First, it uses an auction mechanism – lenders bid in order to lend and accommodate to borrowers seeking smaller scale loans, with the average bid size being just $60. Bids assembled from several lenders are aggregated to create the loan requested by the borrower. Secondly, borrowers can create and use their online social networks for extra exposure by inviting their friends to be part of this marketplace; each borrower’s social network and the actions of their friends being visible to all potential lenders.

The value of hard information

Banks and financial institutions collect data on a large number of variables of interest. Primary among these “hard” credit variables is the credit score (e.g., FICO score). Personal credit scores provide a summary of the borrower’s financial history and are usually available from credit bureaus and rating agencies. Debt?to?income ratios, bank card utilization, number of previous credit inquiries, and time since the first credit line, are some of the other “hard” credit variables that are available to lenders. In addition, banks and financial institutions gather information relating to hundreds of variables such as:

- Demographics (Age, Gender, Education, Location, etc.)

- Family Details (Family Size, Number of Dependents, Age of Dependents, etc.)

- Employment Details (Employer, Years in employment, etc.)

- Financial Details (Income, Net Worth, Assets, Financial Statements, House Ownership, etc.)

- Property Details (Property Type, Location, Condition, Value, etc.)

- Source of lead (Brokers, Direct, Existing Customer, etc.)

The role of social networks in financial lending

Several studies have highlighted the value of an individual’s social network on various transactional outcomes in a number of contexts. Lin et al (2009) study transactions between individual lenders and borrowers in a decentralized online peer?to?peer lending market to answer the following questions.

- Does a borrower’s social network provide information about his creditworthiness and default rates?

- Can a borrower’s likelihood of default be predicted from the default rates in his network?

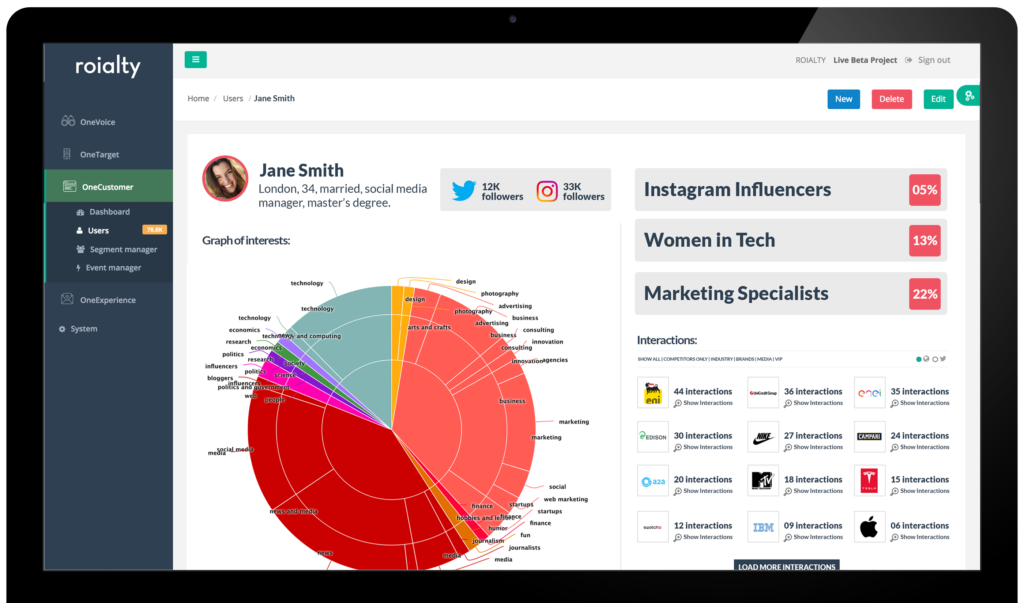

The answer to these question could be represented by ROIALTY: the platform of social behavior and customer segmentation useful to track in real time social interactions to build user’s segments.

Roialty leverages the power of social media data to build a rich social profile of users’ interests and behaviours based on their public interactions and relationships. All interactions, in fact are analyzed and classified in real time against a rich taxonomy (3000+ topics) using proprietary, language-independent algorithms, and directly mapped to profile attributes. Relevant social behaviours are automatically tracked and mapped by ROIALTY’s solutions: One Target, One Voice, One Customer, One Experience.

The figure demonstrates an example of ROIALTY’s Social Profiling platform that depicts the main interests of anonymous users.

What is ROIALTY’s approach for Fintech Market?

Predictive Models

Social data has been proved to be highly effective in predicting socio-demographic attributes and even personality traits. In combination with internal data, Roialty social profile attributes can be used to predict characteristics, preferences and inclinations of customers and prospects (e.g., affluence, propensity score, financial risk, intention to buy and more)

Acting as a proxy for multiple indicators, Roialty’s social profiling can model new users (i.e., cold start problem), allowing recommendation systems to suggest relevant items and offers even in the absence of historical data

Personalisation

Roialty’s dynamic segmentation, content and offers can be personalized in real time along the customer journey (e.g., promoting a car loan to someone who started to interact in the automotive domain)

Roialty profile-driven engagement delivers personalized calls to action across the different channels, providing a more relevant, contextual user experience that increases engagement and loyalty

Triggering & Alerting

Social and other digital behaviours can be tracked to trigger specific business processes

Real-time segmentation can deliver instant updates to other marketing automation systems

Campaign Optimisation

Aggregate analysis of users profiles (audiences) can provide actionable insights to improve customer segmentation criteria, to find and engage the right influencers across different channels and to optimize content based on engagement performance.

Roialty audience insights can be also applied to any other available set of social profiles (e.g. competitor’s followers, users talking about a specific product or topic)

Audiences can be segmented based on specific business criteria or by using a solution’s automatic clustering capabilities. Segments can be used to create tailored and lookalike audiences on the different social media channels to deliver personalized campaigns and optimise social media advertising costs.

Discover how to build a customer segmentation strategy for the Fintech market through social profiling! Download the company overview.